Enter search criteria

Enter search criteria

| International Trade FAQs |

|

From the UK, an export is any product that leaves UK and crosses an international border into another country and an import is a product that crosses the UK border coming into the UK. The IOE&IT run training courses on Importing and Exporting - Click here to find out more .

It is the capital of a business which is used in its day-to-day trading operations, calculated as the current assets less the current liabilities. From an international point of view it would be the capital exporters require to purchase supplies, components, to produce or resell products for sale to international markets. The IOE&IT run training courses on International Finance - Click here to find out more

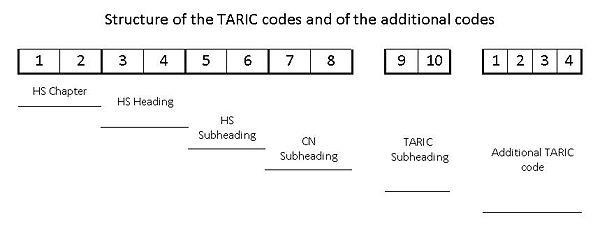

The TARIC code (TARif Intégré Communautaire; Integrated Tariff of the European Communities) is designed to show the various rules applying to specific products when imported into the EU.

The IOE&IT run training courses covering product classification - Click here to find out more The Union Customs Code is the EU legislation which provides the legal basis and generic requirements of EU (including UK) customs formalities. Introduced on 1st May 2016, the Union Customs Code also covers special procedures including Customs Warehousing (CW),Temporary Admission (TA), Inward and Outward Processing. The IOE&IT run training courses which cover the Union Customs Code - Click here to find out more There are many benefits of AEO approval including the following: Do you have questions about AEO assessment? Contact us to find out how we can support you - call 01733 404419 or email events@export.org.uk INCOTERMS (International Commercial Terms) are an internationally recognised set of trade terms developed by the International Chamber of Commerce (ICC). The terms define the responsibilities and liabilities between a buyer and a seller. They cover who is responsible for paying freight costs, insuring goods and covering any import/export duties. The IOE&IT run a training course which covers Incoterms - Click here to find out more There are many different documents required for export, depending on the destinations import requirements, the type of product or whether there is a trade agreement in place. For advice on documents for different products and destination please contact the IOE&IT Helpline. The IOE&IT run training courses which cover import and export documentation - Click here to find out more

The Institute of Export & International Trade's mission is to enhance the export performance of the United Kingdom by setting and maintaining professional standards in international trade management and export practice. This is principally achieved by the provision of education, training and practical business support services. The challenging and often complex trading conditions in international markets mean that our role has never been more vital. The Institute continues to be committed to the belief that real competitive advantage lies in the competence of British businesses. Our future export growth must be underpinned by a sound foundation of knowledge. Click here to find out more about what the Institute of Export & International Trade can do for you

It would be considered an export of a service and it depends on how the software is delivered. There are three main categories that are tangible software, downloaded software, and software accessed via the cloud. Tangible software refers to instances where a technology product is sold to a customer in a box or C.D, or memory stick. Downloaded software refers to is a software license that allows a customer to download a tech tool directly to their local hard drive and then use the software for whatever application they have purchased it for, like music software recording. Please note that Licence costs are included in the WTO methods of valuation for import duty. Software accessed via the cloud accounts for “Software As A Service” (SaaS) product. This type of software is where a customer accesses it over an Internet connection via the cloud for example. The big issue for SaaS products are the tax implications, for example in the EU, there is a requirement to be registered for VAT , for companies supply consumers, even if the company is not based in the EU and the US is the same with different state taxes. The IOE&IT can help guide you through selling services overseas - Click here to find out more Rules of origin are used to determine the origin of a product for purposes of international trade. For example, the EU and Canada have a preferential trade agreement, so for exporters they need to prove their products being shipped meet the rules of origin so that the importer can benefit from reduced or zero import duties. In the case of an EU company they have to comply with rules to state that their product has EU origin. The IOE run training courses covering the Rules of Origin - Click here to find out more For countries where the EU has preferential trade agreements, an EUR1 is required so that it confirms the goods shipped from the EU complies with the rules to be considered as being of EU origin and the products can have preferential import duty applied to them. The IOE run training courses covering the EUR1 Document - Click here to find out more An ATR1 document enables goods to qualify for tariff preferences on imports and exports between the EU and Turkey. More information on ATR’s can be found in Customs Notice 812. The IOE run training courses covering the ATR1 Document - Click here to find out more An EC Certificate of Origin is a non-preferential document that certifies what the origin of the products is in a shipment. This may be requested by a client or for import compliance. For example, textiles shipped from the UK to Argentina require an EC Certificate of Origin. An EUR1 is used for countries where the EU has preferential trade agreements, an EUR1 is required so that it confirms the goods shipped of EU origin and the products can have preferential import duty applied to them. The IOE run training courses covering Certificates of Origin - Click here to find out more Supplies of goods sent to the Channel Islands are regarded as exports for VAT purposes and may be zero-rated if the following conditions of proof of export are met: • The goods are exported from the EU within the specified time limits • The exporter has official or commercial evidence of export • Comply with Customs Notice 703 where details on the above requirements are listed The IOE run training courses on International Finance - Click here to find out more An indirect export is a shipment that is shipped from the UK to another EU country, and then shipped from that EU country outside the EU. The IOE run training courses covering definitions of Exports - Click here to find out more The Single Administrative Document (SAD) which is also known as a C88 in the UK is a form for declaring import, export, transit and community status declarations with UK Customs. The IOE run training courses on Customs Compliance - Click here to find out more When using EX Works all of the costs and risks of shipping the goods are for the buyers account. For the buyer it can be a good term to get a clear picture of all of their shipping costs, which can help calculate more accurate landed costs. However, there are issues when using EX Works. For example the risk passes when the goods are made available for collection. This means that the buyer is responsible for loading the goods, but many companies who use this term as the seller, will actually load the goods. The other issue is the customs declaration for export, where the buyer has responsibility for this process, yet a seller who is exporting from the UK, would not be charging VAT. Therefore, it is important that they can get proof of export for HMRC audit purposes, which can be difficult in some cases when using the EX Works term. For an exporter it may be better to use other terms, which cover the loading and export declaration process. The IOE run training course on Incoterms - Click here to find out more The volume of a shipment is calculated by multiplying the Width by the Height by the Depth. The volume is used by Freight Forwarders to calculate the cost of a shipment and below is a rough guide on the volume to weight equivalence they use to determine costs. • Air Freight - EQUIVALENCE: 1 Cubic Metre = 167Kg • Road Freight - EQUIVALENCE: 1 Cubic Metre = 300Kg • Sea Freight - EQUIVALENCE: 1 Cubic Metre = 1,000Kg The IOE run training courses covering export packing and shipping - Click here to find out more An Arab Certificate of Origin is a non-preferential document that certifies what the origin of the products is in a shipment. This may be requested by a client for import for countries in the Arab League which are: Algeria, Bahrain, Comoros, Djibouti, Egypt, Iraq, Jordan, Kuwait, Lebanon, Libya, Mauritania, Morocco, Oman, Palestine, Qatar, Saudi Arabia, Somalia, Sudan, Syria, Tunisia, United Arab Emirates, Yemen. The IOE run training courses covering the Arab Certificate of Origin - Click here to find out more The EU has a trade agreement with South Korea, enabling preferential trade. However, for shipments over 6000 Euros, normally a EUR1 would be issued to certify the goods meet the rules of origin. However South Korea does not accept the EUR1 form. For preferential trade with South Korea, then Approved Exporter Status is required to enable preferential import duty. To apply for this, you need to complete a C1454 form and once approved you would use your Approved Exporter Number for your customer to benefit from preferential. Import duties. The IOE run training courses covering preferential trade - Click here to find out more Delivered Duty Paid (DDP) is a term where the seller is responsible for the import duties and taxes of the shipment in the country of import. If a company is aware that these charges would be for their account and doesn’t impact on the profitability, then may be the company would opt to use this term. However, in the majority of B2B shipments, this can result in charges for the seller that would impact on profitability, due to a lot of “unknown” costs that could be applied to the sellers account. Another issue is that some countries require the buyer to be registered as an importer in the country of import, which restricts the use of this term. For example you cannot ship goods DDP to Russia with DHL. The IOE run training course on Incoterms - Click here to find out more An ATA Carnet is an international Customs document which allows the temporary importation of commercial samples, professional equipment or goods for an exhibition. An ATA Carnet is valid for one year and allows for movement of the goods shown on the Carnet as many times as required during the 12 months to any of the destinations applied for. An example of the use of an ATA Carnet is Formula 1 team’s use these when then go to different countries to compete in the Grand Prix. The IOE run training courses covering ATA Carnets - Click here to find out more When goods are exported from the UK, these are shipments that go to destinations outside the European Union. VAT is not charged on Export shipments, therefore, proof of export is required for HMRC audit purposes. The IOE run training courses covering proof of export - Click here to find out more This is OK to do as the export declaration to UK customs does allow for this. The only issue from the commercial point of view is the exchange rate as fluctuations can result in reduced profitability. Also, receiving payments in US Dollars into your bank can carry charges, which again may affect the profitability of the transaction. The IOE run training course on International Sales & Marketing - Click here to find out more For all Incoterms, a good rule is to write the Incoterms as follows: • Incoterm + Place + Version In the case of FOB, the reason why it is important is that earlier versions of Incoterms rules can be used if specified and there is a different point at where the risk transfers from the 2000 version to the 2010 version. The IOE run training course on Incoterms - Click here to find out more A customs procedure code (CPC) is a code used on import and export declaration, which identifies the customs process which goods are being entered into and removed from. The IOE run training courses covering Customs Procedure Codes - Click here to find out more Under the new Union Customs Code (UCC) and customs special procedures, you do have to be authorised to use Inward Processing. This is either Authorisation by Declaration, if you only use the procedure up to 3 times a year, or Full Authorisation for use of more than 3 times a year. The UCC came into force on 1st May 2016, so authorisations for Inward processing relief that were granted prior to that date can still be used until the authorisation needs renewing. The IOE run training courses covering the Union Customs Code - Click here to find out more

|